For small congregations, every dollar matters. Between maintaining a building, supporting community outreach, and funding ministries, there is little room in the budget for unexpected expenses. Yet one essential cost cannot be overlooked: insurance. The question every church board eventually asks is, who offers the lowest insurance rates for small houses of worship without sacrificing the coverage needed to protect the congregation, volunteers, and property?

The answer is not as simple as naming a single provider. Insurance rates vary significantly based on location, building age, activities offered, and risk management practices. However, by understanding the marketplace and comparing specialized carriers, small churches can secure affordable protection. This guide examines the current cost landscape, profiles the leading insurers for religious organizations, and provides actionable strategies to lower premiums while maintaining comprehensive coverage.

Understanding the Current Insurance Cost Landscape for Small Churches

Church insurance is not a one‑size‑fits‑all product. Small churches typically those with fewer than 150 regular attendees face a wide range of potential premiums. According to recent industry data, annual insurance costs for small congregations generally fall between $1,200 and $7,500 per year. This broad range reflects the many variables that insurers evaluate when pricing a policy.

On a national average basis, churches in the United States spend approximately $500 to $740 per year for a comprehensive business insurance package, which breaks down to about $41 to $62 per month. These figures represent general averages; actual premiums can be higher or lower depending on the specific risk profile of each house of worship. For instance, a small rural church with a newer building, limited programs, and a clean claims history will likely pay far less than a similarly sized urban congregation that runs a daily preschool, operates church vans, and offers pastoral counseling services.

It is also worth noting that the church insurance market has experienced significant turbulence in recent years. Major providers such as Church Mutual, GuideOne, and Brotherhood Mutual have been forced to raise rates or, in some cases, drop coverage entirely for certain properties, particularly those in disaster‑prone regions. This shifting landscape makes it more important than ever for small congregations to shop carefully and work with agents who understand the unique needs of religious organizations.

Key Factors That Determine Your Church’s Insurance Premium

Before choosing an insurance provider with the most competitive rates, it’s essential to understand what actually drives insurance costs for small houses of worship. Insurers evaluate many variables, but the following factors have the greatest impact:

1. Property Value and Building Condition

The replacement cost of your church buildings—such as the sanctuary, fellowship hall, and auxiliary structures—is a major factor in determining premiums.

Older buildings with outdated electrical systems, aging roofs, or limited fire protection are considered higher risk and typically result in higher premiums. On the other hand, well-maintained properties with documented upgrades (like modern wiring, fire alarms, and sprinkler systems) are more likely to qualify for lower rates.

2. Ministries and Activities Offered

Every program your church operates introduces a level of liability exposure.

Activities such as:

- Youth and children’s ministries

- Daycare services

- Counseling programs

- Homeless outreach

- Sports leagues

- Mission trips

all increase the potential for claims. Insurers will assess both on-site and off-site activities when calculating your premium.

3. Abuse Prevention and Child Safety Policies

This is now one of the most critical factors influencing church insurance costs.

Insurance carriers favor churches that implement strong risk management practices, including:

- Annual background checks for staff and volunteers

- A strict two-adult rule for children’s activities

- Classroom monitoring systems

- Secure check-in and check-out procedures

- Formal volunteer training programs

Stronger safeguards reduce risk and can significantly lower premiums.

4. Claims History

A church’s claims history plays a major role in pricing.

Organizations with a clean record typically receive better rates, while those with prior claims—such as slip-and-fall incidents, vehicle accidents, or misconduct allegations—may face higher premiums for several years.

5. Location and Regional Risks

Geographic location directly impacts insurance costs.

Churches in areas with:

- Higher crime rates

- Increased litigation risks

- Exposure to natural disasters (hurricanes, floods, wildfires, tornadoes)

often pay more for both property and liability coverage. In high-risk regions, some insurers may even limit or decline coverage.

6. Vehicles and Transportation

If your church owns vans or buses, this adds another layer of risk.

Insurers evaluate:

- Driver qualifications and training

- Vehicle maintenance records

- Transportation safety policies

Strong management practices in this area can help control commercial auto insurance costs

Comparing the Leading Providers for Small Houses of Worship

Several insurance companies specialize in serving religious organizations. Each has distinct strengths, and the “lowest rate” will depend on your congregation’s unique characteristics. Below is an overview of the major players.

1.GuideOne Insurance

GuideOne is widely recognized as a top provider for church insurance. The company offers a comprehensive package called FaithGuard, which combines property and liability coverage into a single policy. GuideOne’s policy comes in three levels—Basic, Broad, and Special—allowing small churches to select the tier that fits their budget and risk profile.

Key features of GuideOne’s church insurance include liability limits up to $5 million aggregate, counseling liability coverage that includes volunteers and lay leaders, coverage for personal effects of volunteers on mission trips, and a broad definition of “insured” that includes volunteers, members, and Sunday school teachers. GuideOne operates in all 50 states through a network of independent agents and maintains an A- (Excellent) financial strength rating from AM Best.

However, GuideOne’s rates may not always be the lowest. A real‑world example from a Louisiana church of about 80 members illustrates this point: after Church Mutual non‑renewed its policy, the congregation switched to GuideOne, and its annual premium increased from $10,692 to $14,050, while the deductible rose from $1,000 to $2,500.

2.Church Mutual Insurance

Church Mutual has been insuring religious organizations for over a century and is one of the largest specialty carriers in the space. The company offers customized policies for churches of all sizes, with coverage options including property, general liability, sexual misconduct liability, pastoral counseling liability, and commercial auto.

Church Mutual is rated A by AM Best and provides access to risk management resources that help churches reduce their exposure. The carrier has a strong reputation for customer service and claims handling.

That said, Church Mutual has faced challenges in recent years. The company has non‑renewed policies in certain high‑risk areas, including parts of Texas and Louisiana, citing changing underwriting appetites. For churches in those regions, securing coverage through Church Mutual may no longer be an option, and alternative carriers must be found.

3.Brotherhood Mutual

Brotherhood Mutual is another leading specialty insurer for churches and religious organizations. The company is particularly well‑suited for congregations that engage in mission trips, as it offers both individual and group coverage for short‑term missions. Brotherhood Mutual also provides comprehensive property, liability, and workers’ compensation coverage tailored to faith‑based organizations.

4.Specialty Programs and New Entrants

Beyond the traditional big three, several other options deserve consideration:

- Convelo offers a select program tailored to small and mid‑sized churches, with core packages including property and liability endorsements up to $5 million total insured value per building and $10 million per policy, plus equipment breakdown coverage and pastoral counseling. This program is written through Church Mutual, so pricing may be similar, but Convelo provides an additional distribution channel.

- Mennonite Mutual provides a Stewardship Protection Program that allows churches to design tailored, cost‑effective coverage. The Ministry Assistance Program has a minimum premium of $500, with a $400 minimum for claim‑free policyholders, and deductibles ranging from $500 to $10,000. This can be an attractive option for very small congregations seeking budget‑friendly coverage.

- Ategrity Specialty Insurance recently launched a pre‑priced platform for religious organizations, having pre‑qualified and pre‑priced more than 200,000 religious institutions across the United States. Small‑business partners can generate quotes in as little as 90 seconds through its data‑driven underwriting platform. While Ategrity is a newer entrant to this niche, its technology‑focused approach may yield competitive rates for straightforward risks.

- Kinsale Insurance provides small property coverage up to $5 million in total insured value with deductibles as low as $500. Kinsale has maintained a consistent appetite for religious organizations, even those that have been non‑renewed by other carriers, making it a valuable option for churches that have struggled to find coverage.

- Heffernan Insurance Brokers is an independent agency that works with multiple carriers specializing in church and nonprofit insurance. By accessing a panel of insurers, Heffernan can shop for the most competitive rates on behalf of each congregation.

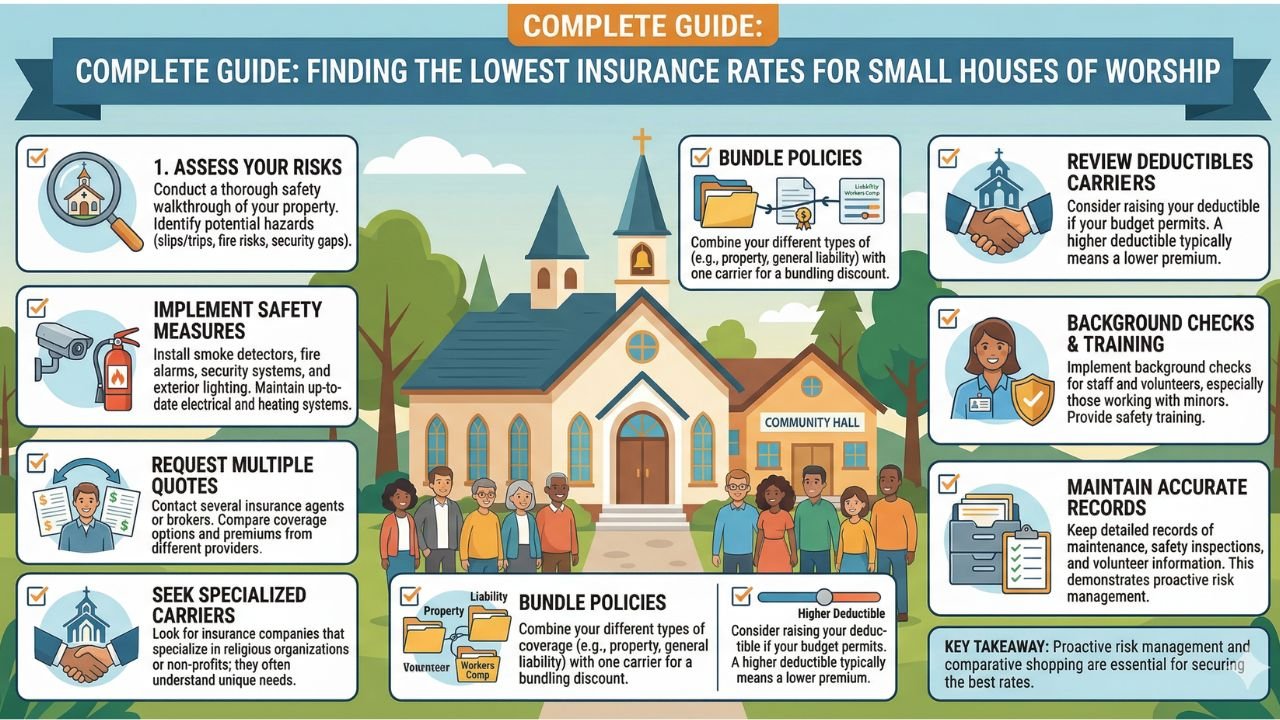

Practical Strategies to Lower Your Church Insurance Premiums

Even after selecting a competitive insurance provider, small congregations can take proactive steps to further reduce their premiums. The key is simple: lower risk = lower cost. Insurers reward churches that demonstrate strong safety, governance, and operational discipline.

1. Strengthen Child Safety and Abuse-Prevention Policies

This is one of the most influential factors in modern church insurance pricing.

To reduce risk and improve insurability:

- Conduct annual background checks for all staff and volunteers

- Enforce a strict two-adult rule for children’s programs

- Implement secure check-in and check-out systems

- Document all volunteer training

- Maintain clear procedures for reporting concerns

Churches with robust, documented safeguards are seen as significantly lower risk—and often qualify for better rates.

2. Improve Property Maintenance and Safety

Well-maintained facilities signal strong risk management to insurers.

Focus on:

- Routine electrical inspections

- Roof maintenance and repair logs

- Working fire extinguishers and alarm systems

- Clearly marked exits and emergency lighting

- Playground safety inspections

- Slip-and-fall prevention (mats, signage, cleaning logs)

Consistent upkeep not only prevents claims but also strengthens your position during underwriting.

3. Implement Strong Driver and Vehicle Safety Protocols

If your church operates vans or buses, transportation risk becomes a major cost factor.

Best practices include:

- Maintaining detailed vehicle service and inspection records

- Creating written transportation policies (especially for youth)

- Enforcing seatbelt use and passenger limits

- Keeping an approved driver list

- Conducting regular background checks and motor vehicle record (MVR) reviews

These steps can significantly reduce commercial auto premiums.

4. Bundle Your Insurance Policies

Many insurers offer discounts when multiple coverages are combined.

By bundling:

- Property insurance

- General liability

- Commercial auto

with one carrier, churches can often unlock meaningful cost savings while simplifying policy management.

5. Right-Size Property Values and Deductibles

Accurate coverage limits are essential for controlling costs.

- Over-insuring leads to unnecessarily high premiums

- Under-insuring creates serious financial risk

Conduct annual property valuations to align coverage with true replacement costs. Additionally, choosing slightly higher deductibles especially for equipment or property damage can lower premiums without compromising liability protection.

6. Work with a Church-Focused Independent Agency

Not all insurance agents understand the unique risks churches face.

Specialized agencies are better equipped to handle:

- Pastoral counseling liability

- Abuse-prevention compliance requirements

- Multi-property or multi-campus coverage

- Church transportation risks

- Volunteer vs. employee liability distinctions

An experienced, church-focused broker can match your ministry with the right carriers and negotiate better pricing on your behalf.

Finding the lowest insurance rates for a small house of worship requires research, comparison, and proactive risk management. While GuideOne, Church Mutual, and Brotherhood Mutual remain the dominant specialty carriers, newer options like Mennonite Mutual, Kinsale, and Ategrity provide competitive alternatives that may better suit certain congregations.

The most important takeaway is this: do not accept the first quote you receive. Insurance markets are dynamic, and carriers’ appetites change over time. By obtaining multiple quotes, strengthening your church’s safety protocols, and working with an independent agent who specializes in religious organizations, you can secure affordable, comprehensive coverage that protects your ministry without breaking your budget.

Your congregation’s mission is too important to be jeopardized by inadequate insurance or unaffordable premiums. Take the time to shop wisely, and you will find a policy that fits both your needs and your finances.